This purpose of this document is to provide the reader with an understanding of the dynamics of this business by retrieving the market trends behind the numbers. While the numbers will change every year, the marketing trends will last for some years.

All the data are reliable but not 100% accurate all the more that they slightly differ according to the sources but forgiving some estimates, the meanings of the numbers are true.

The data have been provided mainly by the IMM Carrara and the MIA.

In 2014 the worldwide trading of stone has reached about 90 millions tons for 24 Billions $ which is about the size of the chewing gum market.

The international business - the imports (or the exports) – account for 55% of the volume. Over the last 15 years, the volume of the international trade has been tripled.

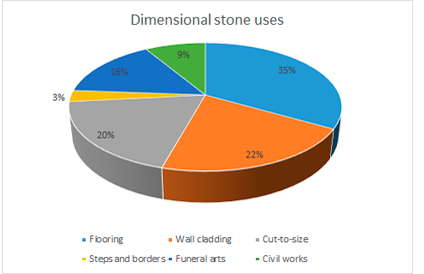

About 75% of the stone processed in the world is used in construction:

And the other 25% are:

The main supply of the stone comes from quarries located in a few countries: China provides 31% of the volume, India 14%, Turkey 10%, Brazil 6%, Italy 5%, Iran 5%, Spain 4% and Egypt 3%.

China is leader with about 35% share but holds next to 50% of the granite market. China processes about 70% of the Indian granite. China has a 48% share of the exports of processed stone.

Italy comes after with a 13% share obtained through high-added value products but Italy position is declining.

Then comes Turkey with a 12% share but only 10% on processed stone. Yet Turkey is on a growing trend. About 80% of the raw stones produced in Turkey are exported to China. Turkey is the largest supplier of stone to China with about 800 M $, India being the second with 500 M $.

India gets an 11% overall share but only 7% for processed stone and Brazil a 7% share but only 5% on processed stone.

The commerce classification regroups the stones in two categories:

The calcareous stones encompass limestone, marble and travertine while the siliceous stones group is made of granite, basalt, sandstone and quartzite.

Let’s review an example of each stone:

In the past 15 years, the volume of the import/export of raw calcareous stones have been multiplied by 7 while it was multiplied by 1.7 for raw siliceous stones.

Calcareous stones represent 55% of the whole stone business. The strong net development of this category has been fostered by

The growing importance of calcareous stone will be further fueled by the richness of options that can be provided by Middle East countries and Iran if the political situation allows it. Egypt is already a significant producer exporting about 3 Mons tons of limestone mainly in blocks to China.

A few words about slate. In the same 15 years, the trade volume of slate has grown by 1.6, slower than the other stones but it has been steady for the last 10 years. This volume is strictly related to the traditional use of slate as roofing tiles which is losing ground.

Whereas the quarrying is quite concentrated, the use of processed stone is very widespread all around the world, but there are some major consumption markets: USA 15%, South Korea 11%, Germany, Saudi Arabia and Japan all with 5% share.

The USA are the largest consumers of Brazilian granite. They import about 700 Mons $ of processed granite from Brazil. They are also the first client of Turkish marble and travertine for 400 M$.

1 Flooring accounts for more than 1/3 of all the stone used around the world. The use of stone in flooring has been multiplied by 2.5 over the past 15 years. It will keep on growing because of two competitive factors:

2 The volume generated by the use on wall cladding have more than tripled over the last 15 years driven by a booming trend of interior wall cladding. Interior wall cladding moves about 9 M tons. This trend will be carried on. It is promoted by all the pre-assembled products such as:

These products are all made in Asia and they consist in transferring the labor cost from the expensive consumption markets to the cheap producing countries since the time-consuming part of the installation is made at the source.

3 The growing importance of cut to size items (and steps and borders) – the volume has been multiplied by 6 in 15 years – is supported by 3 characteristics of the stone industry:

Conclusion : Over the last 25 years, the emerging countries – China first but also Brazil, India and Turkey – have deeply changed the business of natural stone:

Yet, stone being a natural material, all professionals know that there is not a single piece of stone equal to another. This market will never be a “commodity” market; it will always require knowledgeable actors and continuous control.

CONTACT

Tel/ WhatsApp: +84386933979

tony@rockandstone.vn

https://www.facebook.com/worldofstoness

Yen Bai Industrial Park, Yen Bai City, Vienam